Opendoor's Q3'2023 Earnings Estimate & 7 reasons we think Q4 consensus is flat out wrong

Written by

Tyler Okland

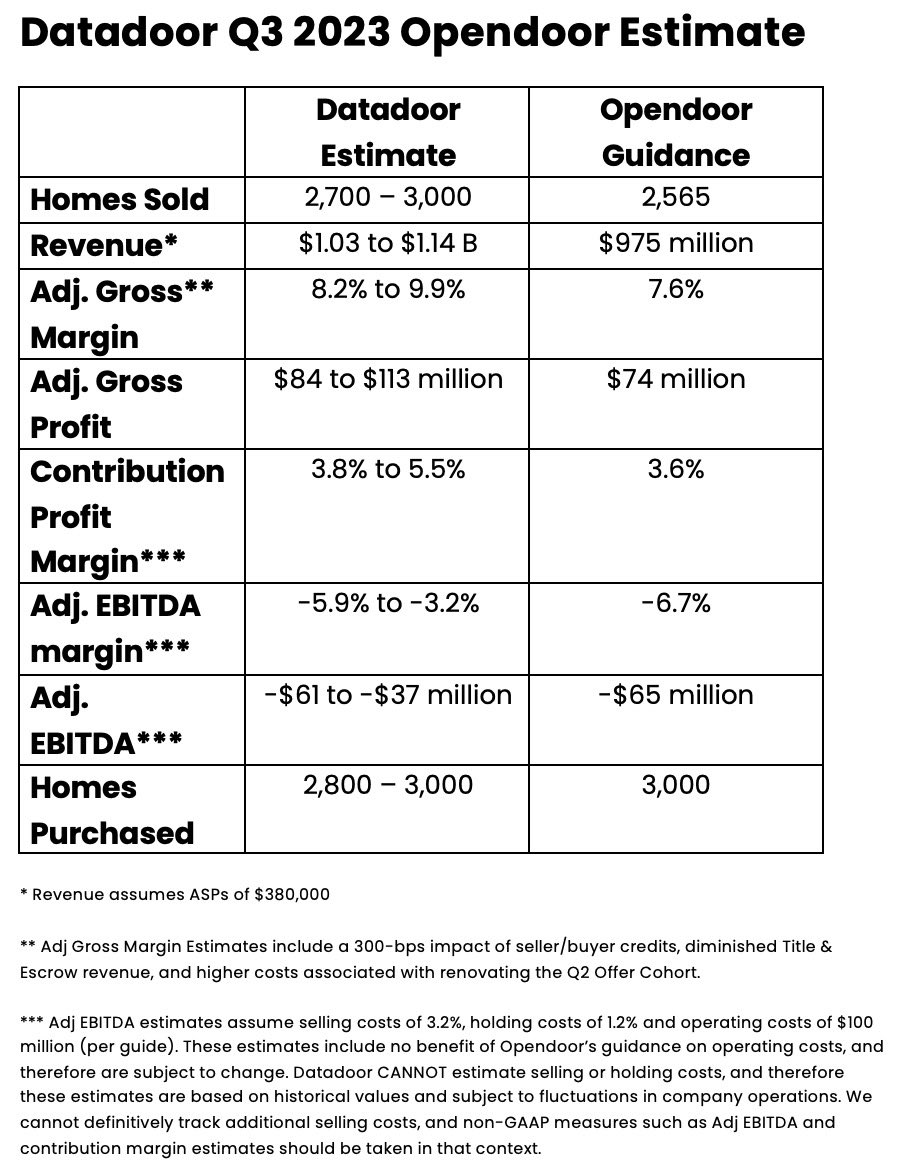

Here's our numbers and 7 reasons we think consensus is flat out wrong.

High level we expect small beats on revenue and adjusted gross margin relative to guide. That said, resale volume is at a low for the year and we expect the year to close at a similar level. It follows that Opendoor will guide for Q4 revenue lower than consensus ($1.15 B).

Consensus Q4 estimates of $1.15 B makes little sense in the following context:

1.) Q4 seasonality -- generally a depreciating season, so no incentive to ramp resale here (the incentive is to ramp in Q1-2, when homes appreciate).

2.) Inventory build up -- can't ramp sales without first ramping acquisions. We expect acquisition ramp in Q4-Q1, hasn't happened in Q3.

3.) Highest mortgage rates in a generation causing...

4.) Transaction volume similar to the GFC. Tough landscape to grow volumes.

5.) Management's stated goal of $10 B revenue run rate in 2024 -- means incentive is actually to push all sales possible into 2024 to thread those goalposts.

6.) Opendoor historically guides for 10-20% lower rev than they actually post. So even if they were going to hit $1.15 B, the guide would be $150 million lower.

7.) The best data on the planet, our data, Datadoor, says $1.15 B is too high an estimate for Q4.

Remember following Q2 earnings $OPEN sold off because rev guide was far lower than consensus.

For those who understand the thesis, Q4 revenue is irrelevant (as was Q2-3), and should not move the stock. Here's all that matters:

1.) Acquisition ramp in Q4-Q1 at decent spreads

2.) Further structural improvements in making boring 1P transactions

3.) Growth in partnerships channels (low CAC)

Institutional Grade iBuying data.

For Everyone.

Create an account to get access to Opendoor data and analysis.

Create an accountJoin the discussion

Continue the conversation about this article in our Discord community.

Join our Discord