Q2'2023 Earnings Estimates: Opendoor Is Breaking Out For a Reason

Opendoor reports Q2 2023 earnings tomorrow after the close. A lot has happened over the past year, and it's our feeling at Datadoor that (after tomorrow) the worst is behind Opendoor.

Let me set the stage:

In the summer of 2022 Opendoor stepped on the gas when they should have pulled the e-brake. There were three unique characteristics that made the housing demand crash of last year so deadly for residential real estate operators.

1.) Fed raised rates at historic pace. You know this one. Historically aggressive rate hikes prompted 30-Year fixed rate mortgage to nearly double from 3% at the start of 2022 to 5.81% in July. Functionally, this increased monthly mortgage payments by 43% in less than 7 months.

This is in the greater context of home prices being up 27.8% in the preceding 18 months. When combining home price appreciation with the change in mortgage rates, the monthly principle and interest (P&I) cost for a home increased by 80% (showing my work: January 2021 home of $300,000 at 2.65% rate P&I of $967/mo. July 2022 home with 27.8% HPA now costs $383,400, 5.5% rate for a P&I of 1,741/mo).

2.) As of July 2022, 90% of mortgaged homeowners had a sub-5% rate. This meant moving became simply irresponsible for 9 out of 10 U.S. homeowners. Coupled with work-from-home tailwinds stymieing job-related moving trends, and both demand and supply evaporated overnight. Nobody listed for sale, and nobody went shopping for homes.

3.) Until it wasn't, the housing market was as hot as it had ever been. This bullet likely deserves a bit more attention.

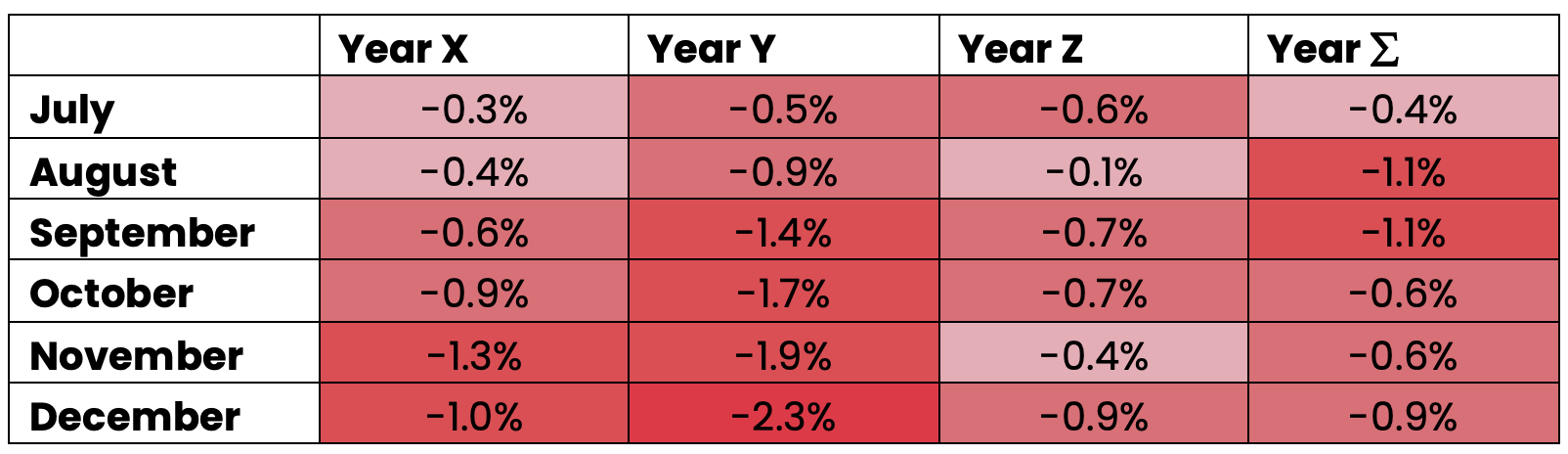

Case-Schiller National Home Price Index, Not Seasonally Adjusted

Above I have graphed the back six months of four of the worst housing years the US has seen since 1975 – note I have hidden the years. Can you guess which is 2022?

Case-Schiller National Home Price Index, Not Seasonally Adjusted

In fact, outside of the Great Financial Crisis, the second half of 2022 was the worst year for U.S. home values in at least fifty years.

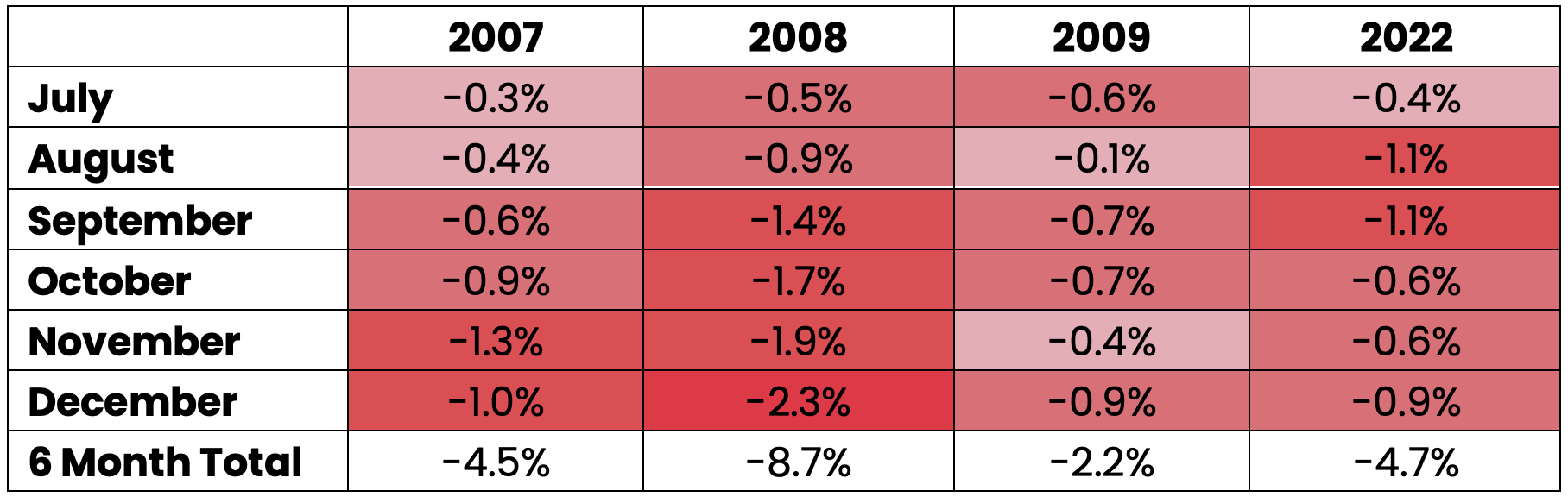

But the speed and amplitude of the declines only tells part of the story.

Perhaps the most important, underdiscussed datapoint is the trend of home values in the 12 months preceding the above housing crashes.

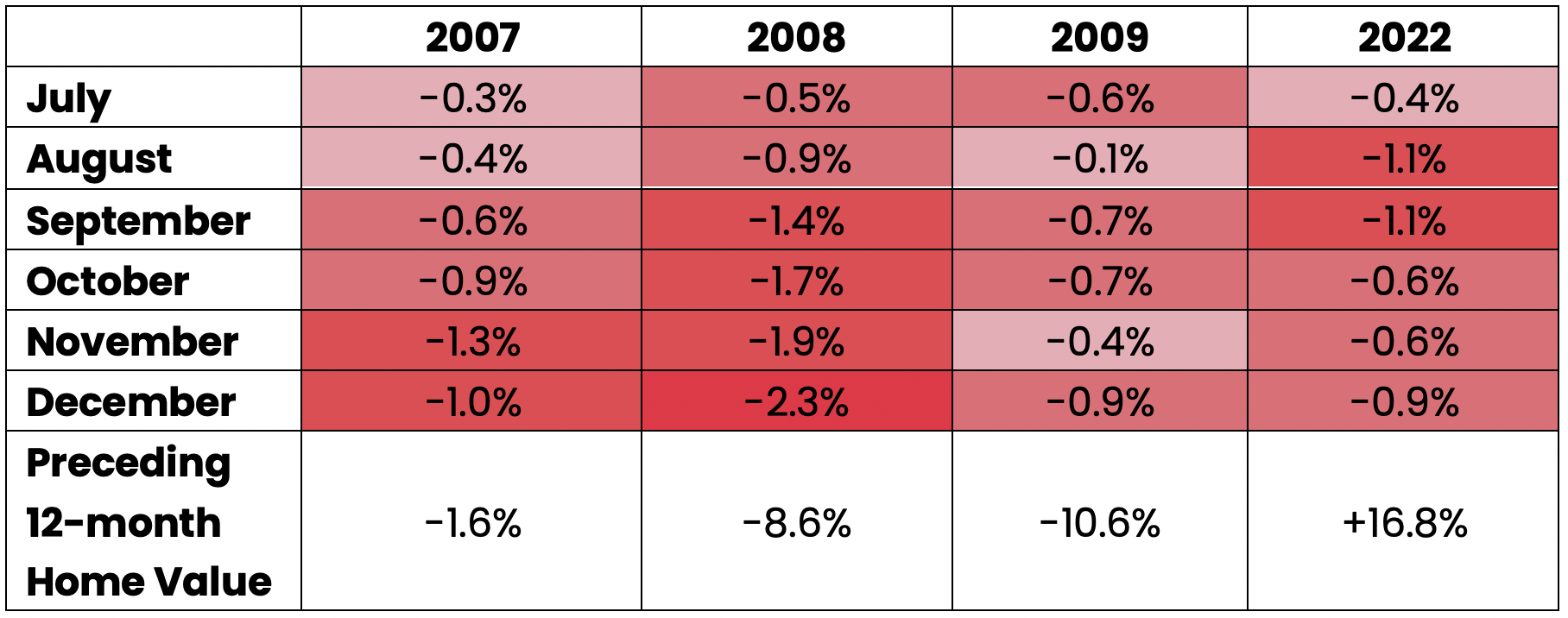

Case-Schiller National Home Price Index, Not Seasonally Adjusted

The housing crash of 2007 – 2010 was not an overnight event, even if that seemed the case. By July 2007 there had already been twelve consecutive months prints at 0% or negative. Leading up to the demand crash of 2022, the US housing market enjoyed an unprecedented gain of +16.8%.

So why was this an issue for Opendoor?

When Opendoor makes an offer on a home, it embeds expected monthly home price appreciation (HPA) in the offer to arrive at a margin target.

For example, if Opendoor expects +1.5% monthly HPA for a particular home, and estimates 3 months to sell, Opendoor may offer the spot price of that home (what the home is valued at right now), plus its 5% fee.

On the resale side, Opendoor can then list the home for its expected value three months from now (+4.5%), and wait for the home to appreciate to that level for sale (5% fee + 4.5% HPA = roughly 10% target gross margin).

Conversely, if Opendoor expects -1.5% monthly HPA, the company would need to offer 10% less than the spot price (This 10% is known as 'spread.' 10% spread plus 5% fee -4.5% home price depreciation). Conversion is lower, but margin can be maintained, even in a down market.

For the year prior to the demand crash of 2022, Opendoor saw month-over-month HPA of 1.5% or higher every month, which meant their offers were coming in quite close to the spot price (sometimes higher). So when housing demand evaporated this past summer those 20,000 homes Opendoor purchased between April and August (the Q2 Offer Cohort, or Q2OC) were immediately worth less than purchase for.

The delta from incredibly hot to irretrievably cold is what made last year’s market so dangerous for Opendoor, and it cost them billions.

Should the company have proceeded more cautiously? Absolutely. Should Opendoor have weighed the aftermath of an aggressive rate hike scenario (in the context of all the above) more seriously? Without a doubt.

That said, I think it’s also important to note that the company did not plan for what happened because it had simply never happened before.

There. I think we’ve set the stage a fair bit.

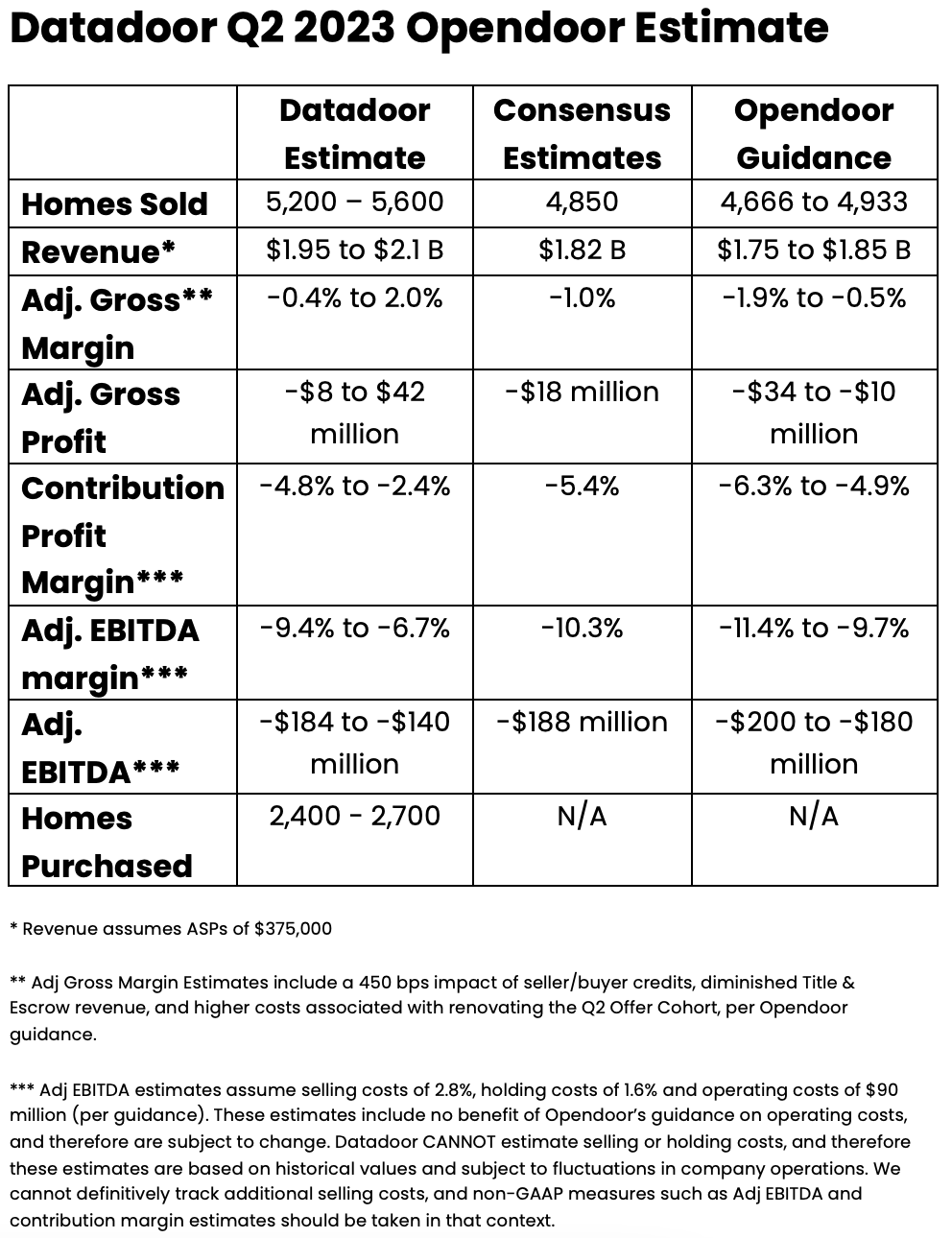

Now let’s talk about data. It's that time where we share our best estimates for the results Opendoor will post tomorrow:

As you can see, we estimate Opendoor will beat on the top and bottom line (Our historical accuracy is publicly available). We break down Opendoor’s operational performance in granularity below.

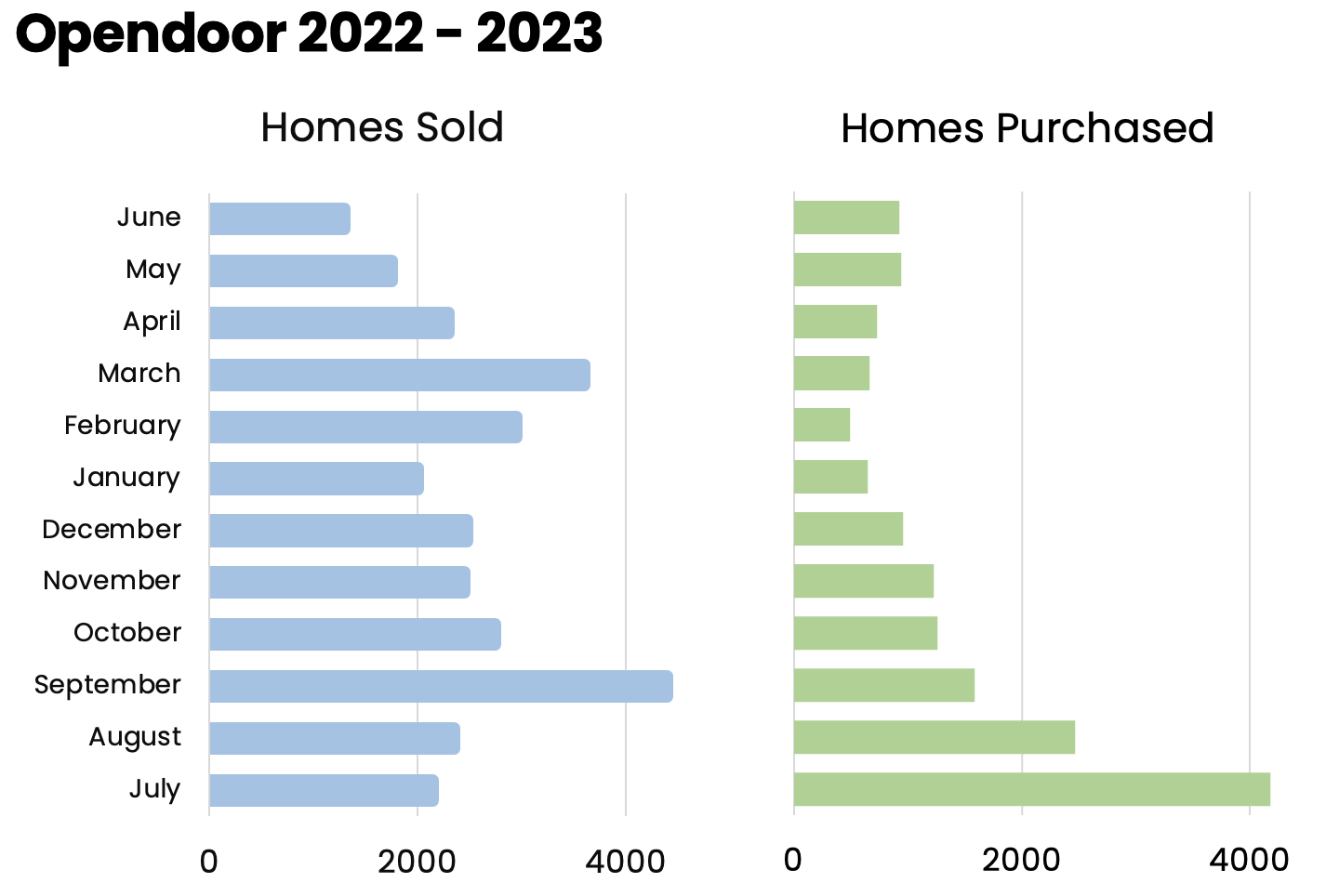

The company has significantly reduced scale (and thereby costs), focusing on offloading existing inventory rather than aggressive acquisition. This has resulted in limited fresh inventory, and therefore lower sales volume.

Opendoor has leaned into ultra-conservative inventory acquisition, offering $0.90 on the dollar for most homes to ensure margin in an unpredictable and otherwise down market. This decreased real-seller conversion from ~35% to 10 – 15% (and nudged customer NPS from 85 to 75), which also contributes to the lower purchase and sales volume.

Opendoor is firmly a net seller of homes since August 2022 (selling volume > purchase volume). This past month (July) that changed, with the company’s existing inventory and total listings rising 10% month over month.

While some (myself included) might question Opendoor’s decision to begin acquiring more homes at precisely the same time they struggled with margins in the two prior years (the Q3 – Q4 housing market is seasonally slower and more likely to see home price depreciation than Q1 – Q2), recent cohort margins are excellent and additional volume is absolutely necessary.

Given the amount of fixed costs embedded in Opendoor’s operations, we estimate the company must generate revenue of $2.0 to $2.5 Billion per quarter at 10% adjusted gross margins to achieve GAAP profitability.

Opendoor is roughly there from a volume perspective for Q2, but nowhere near what is needed for adjusted gross margin (our estimate: -0.4% to 2.0%). And now that Opendoor has sold off the Q2OC, it does not carry enough inventory to crest the volume goalpost to break even for Q3.

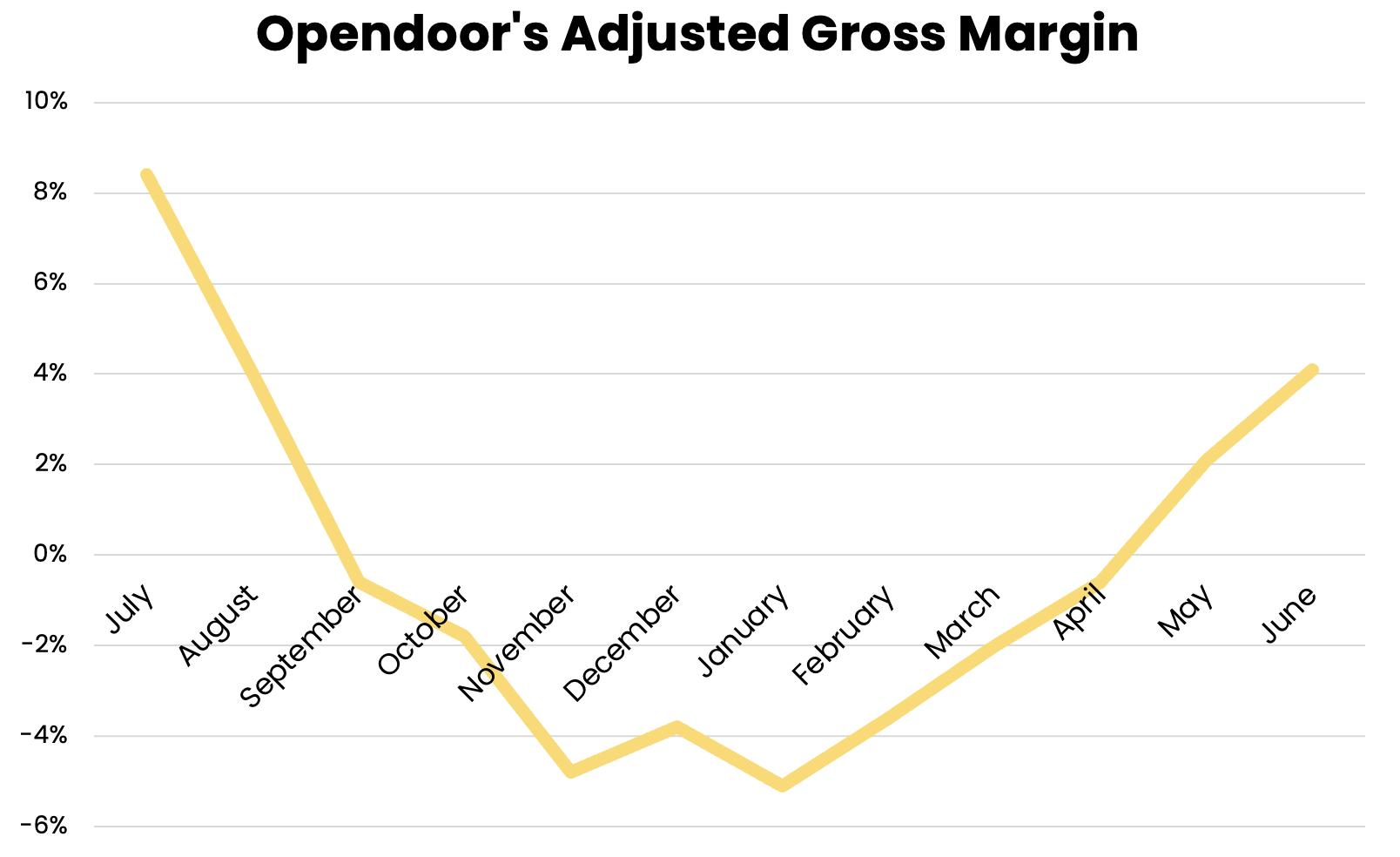

But how is margin trending?

Margin plummeted in the wake of demand destruction, bottoming between November and January as the company poured incentives and renovations into selling the Q2OC.

However, the company has made a hairpin turn since then, climbing out of the trough back towards reasonable unit economics. July margins are > 1,000 bps higher than January's, and heading higher. We expect margins to improve each quarter through 2023, and the early Q3 data corroborate this position.

CEO Carrie Wheeler guided for Q2 adjusted gross margins of -1.2%, and I estimate actual will be between -0.4% and 2.0%.

But the demand crash of 2022 happened nearly a year ago – how is the company still struggling with margin today?

One simple reason: only half of the homes sold this quarter represent fresh inventory (inventory purchased post-Q2 Offer Cohort). And the Q2OC homes sold this quarter were the last of the entire cohort, the most difficult and expensive homes to sell; the lemons. These final Q2OC homes dragged down the margin for the entire quarter.

The good news for those constructive on Opendoor is the company has succeeded in selling off virtually all 20,000 Q2OC homes – with fewer than 100 remaining in inventory today. And post-Q2OC monthly purchase cohorts are faring quite well.

Opendoor has posted double digit adjusted gross margins for every monthly purchase cohort since November, and homes purchased in 2023 have sold for ~15% adjusted gross margins on average. Meanwhile buy-to-list premiums have never been higher for the company, indicating more margin upside ahead.

Closing Thoughts

We've made it our business over the past year to accurately chronicle Opendoor’s operations across all core metrics. Opendoor has offloaded nearly all the toxic inventory that plagued their margins and their capital for the better part of a year. Conservative purchase offers have resulted in a higher-margin business but without sufficient volume to offset fixed costs. However, purchase volumes are steadily ramping.

Opendoor is up 300+% in 2023, and there is a reason the company is breaking out. Opendoor has rebuilt itself with a higher-margin and slightly smaller version of the iconoclastic business that shouldered its way into the spotlight a few years ago. I expect Opendoor will continue to outperform as the Q2OC margin hangover lifts and fresh cohorts are allowed to shine.

Earnings tomorrow. Make sure to join us in our Twitter Spaces for our LIVE post-earnigns discussion!

Institutional Grade iBuying data.

For Everyone.

Create an account to get access to Opendoor data and analysis.

Create an accountJoin the discussion

Continue the conversation about this article in our Discord community.

Join our Discord